Over 60% of UK small business owners admit they wasted money on banking fees they didn’t need to pay. You don’t have to be one of them. Choosing the best business bank account in the UK can save you hundreds of pounds a year — and the good news is, several excellent free options exist right now.

Whether you’re a freelancer just starting, a sole trader building momentum, or someone who’s just formed a limited company, this guide cuts through the noise. You’ll know exactly which accounts to consider, what each one actually offers, and which red flags to avoid. Before setting up your finances when starting out, getting your banking right is one of the smartest first moves you can make.

Do You Actually Need a Business Bank Account?

Technically, sole traders in the UK aren’t legally required to have a separate business account. But operating without one creates real problems — fast.

HMRC expects clear records of your business income and expenses. Mixing personal and business transactions in one account makes your tax return a nightmare. It also signals poor financial management to any lender or investor you approach later.

Limited companies face a different situation entirely. You must keep business finances separate from personal funds by law. Using a personal account for company money is a serious legal violation. To understand which accounts suit each business structure, knowing whether you’re a sole trader or limited company matters more than most people realise.

What Makes a Business Bank Account “Free”?

Free doesn’t always mean free. Many accounts advertise no monthly fees but charge you for every transaction, cash deposit, or overseas payment.

A genuinely free business account has:

- No monthly fee (or a 12-month free trial that clearly states what comes after)

- Free UK bank transfers (sending and receiving)

- No charge for standard payments via Faster Payments

Watch out for accounts that waive the monthly fee but charge 30p–50p per transaction. If you make 100 transactions a month, that’s £30–£50 extra you didn’t budget for. Always check the full fee schedule — not just the headline rate.

The 7 Best Business Bank Accounts in the UK for 2026

Here’s where things get practical. These accounts consistently rate highest for UK small business owners, with a strong focus on free or low-cost options.

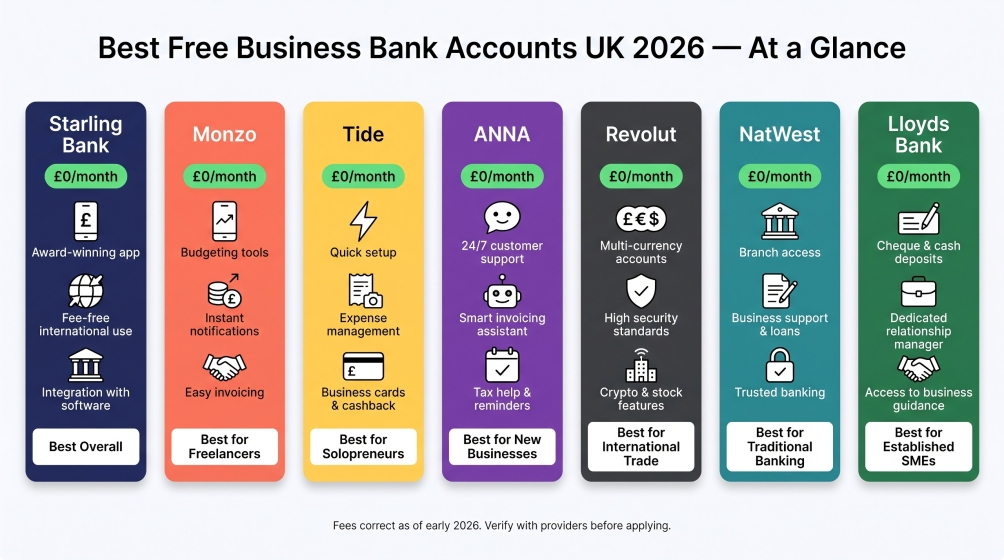

1. Starling Bank Business Account — Best Overall Free Account

Starling remains the gold standard for free UK business banking in 2026. It charges no monthly fee and no fees on UK bank transfers. You get a full current account with a sort code and account number, a Mastercard debit card, and access to an app that genuinely rivals desktop banking software.

What you get free: UK transfers, invoicing tools, accounting integrations (FreeAgent, Xero, QuickBooks), spending categorisation, and 24/7 in-app support.

Downside: No physical branches. Cash deposits cost £3 per deposit via Post Office. If your business handles a lot of cash, this is a meaningful limitation.

Best for: Sole traders, freelancers, consultants, and early-stage limited companies who operate primarily online.

Eligibility: UK resident, business registered in the UK, sole traders and limited companies accepted.

2. Monzo Business — Best for Sole Traders on a Budget

Monzo offers two business tiers. The free Lite plan suits sole traders who want no-frills banking without monthly costs. The Pro plan (£9/month) adds tax pots, integrations, and virtual cards.

The free version handles standard UK payments, gives you a full account number and sort code, and includes basic spending insights. It’s not as feature-rich as Starling’s free tier, but it’s solid for simple sole trader use.

Downside: The free plan doesn’t integrate with accounting software. You’ll export CSVs manually, which adds admin time. Limited company accounts aren’t available on the free plan.

Best for: Sole traders with low transaction volumes who want a recognisable brand and clean app experience.

3. Tide Business Account — Best for Fast Setup

Tide gets you a verified business account in under 10 minutes in most cases. It’s designed specifically for small businesses and self-employed people who need to get banking sorted quickly.

The free plan includes a business Mastercard, UK bank transfers (though note: 20p per transfer on the free tier), and expense categories. Paid plans start at £9.99/month and include unlimited free transfers.

Downside: The free plan charges 20p per UK transfer, which adds up if you invoice frequently. It’s not a “pure” free account in the same way as Starling.

Best for: Businesses that need speed of setup and are happy to pay a small per-transaction fee or upgrade quickly.

4. ANNA Money — Best for Invoicing Built-In

ANNA (Absolutely No Nonsense Admin) combines a business account with invoicing and tax reminder tools in one app. The Pay As You Go plan charges no monthly fee but takes 20p per UK payment and 1% on card payments.

The real draw is the built-in invoicing feature. You can create and send invoices, chase payments, and track what’s outstanding — all inside the banking app. For freelancers who hate admin, that’s a genuine time-saver.

Downside: Per-transaction fees mean it’s not truly free at volume. The interface is fun and colourful, but some users find it less serious-feeling for client-facing tasks.

Best for: Freelancers, creatives, and consultants who invoice regularly and want to cut admin tools.

5. Revolut Business — Best for International Payments

If your business deals with overseas clients or suppliers, Revolut deserves a serious look. The free plan includes multi-currency accounts, competitive exchange rates, and international transfers at interbank rates (with limits).

You can hold money in 25+ currencies. The free plan includes five free international transfers per month and 10 free team members.

Downside: The free plan has a fair usage limit on currency exchange (£1,000/month). Beyond that, you pay a 0.5% fee. Customer support on the free plan is slower than premium tiers.

Best for: Import/export businesses, digital agencies with overseas clients, or UK businesses billing in euros or dollars.

6. NatWest Business Banking — Best Traditional Bank Free Trial

If you prefer a high-street bank with physical branches, NatWest currently offers 2 years of free business banking for startups and businesses switching in 2026. After the free period, standard fees apply (around £8–£10/month).

You get a dedicated relationship manager option, branch access, and CHAPS payments. The full-service offering appeals to businesses that need face-to-face banking.

Downside: Free period ends. After year two, you pay. The app experience lags behind digital-first competitors. Cash handling is easier, but the app feels dated compared to Starling or Monzo.

Best for: New limited companies that want traditional banking infrastructure and plan to review accounts after the free period ends.

(According to Which? Business Banking, NatWest consistently scores well for branch access and dispute resolution among traditional UK business banks.)

7. Lloyds Bank Business Current Account — Best for Growing SMEs

Lloyds offers an 12-month free trial for businesses with a turnover under £3 million. After the trial, it costs £8.50/month. The account includes a full current account, overdraft facilities, and access to business loans and finance.

For a business expecting to grow into credit facilities, loans, or a commercial mortgage, having a relationship with a major high-street bank from the start has real long-term value.

Downside: Free period is only 12 months, shorter than NatWest’s offer. The digital tools aren’t as slick as digital-first banks.

Best for: Small businesses with growth ambitions that want access to finance products in the near future.

Side-by-Side Comparison: Free Business Accounts at a Glance

| Account | Monthly Fee | UK Transfers | Cash Deposits | Best For |

|---|---|---|---|---|

| Starling Bank | £0 | Free | £3 via Post Office | Most businesses |

| Monzo (Lite) | £0 | Free | Not available | Sole traders |

| Tide (Free) | £0 | 20p each | Not available | Fast setup |

| ANNA (PAYG) | £0 | 20p each | Not available | Invoicing |

| Revolut (Free) | £0 | 5 free intl/month | Not available | International |

| NatWest | £0 (2 years) | Free | Yes (branch) | Traditional banking |

| Lloyds | £0 (12 months) | Free | Yes (branch) | Growing SMEs |

Fees correct as of early 2026. Always verify directly with the provider before opening an account.

What to Look for Beyond the Monthly Fee

Most beginners focus entirely on the monthly fee. That’s understandable — but it’s not the whole picture.

Here are the factors that actually affect your day-to-day experience:

Transaction limits: Some free accounts cap the number of monthly transactions before charging. Tide’s free plan, for instance, charges per transfer from day one.

Accounting software integration: If you use Xero, QuickBooks, or FreeAgent, check whether your bank connects directly. Manual CSV exports eat hours you don’t have.

FSCS protection: The Financial Services Compensation Scheme protects eligible deposits up to £85,000. Most major UK banks are covered. Verify this before depositing large sums with any challenger bank.

Overdraft access: Free accounts rarely include overdrafts. If you need credit flexibility, factor in whether the bank offers business overdrafts and at what rate.

Customer support quality: Digital-only banks are getting better, but if something goes wrong with a payment, you want to reach a human quickly. Read recent Trustpilot reviews — not just the headline score, but the 1-star complaints to see what fails most often.

The Mistake Most New Business Owners Make

The biggest error isn’t choosing the wrong account. It’s waiting too long to open one at all.

Many sole traders run their first 6–12 months through a personal current account. That creates a tangled mess of personal and business transactions that takes days to separate at tax time. The stress — and the risk of missing deductible expenses — is entirely avoidable.

Open a dedicated business account on day one. Even if you choose a free account today and switch later, the habit of keeping business and personal finances separate saves you significant time and money every single year.

The Federation of Small Businesses consistently reports that poor financial record-keeping is one of the top administrative burdens for UK small business owners — and it’s one of the easiest to fix with the right setup from the start.

How to Switch Your Business Bank Account in the UK

Switching feels daunting. In reality, it’s straightforward for most businesses.

The Current Account Switch Service (CASS) covers many business accounts. It moves your standing orders, direct debits, and incoming payments automatically within 7 working days. You don’t need to notify every contact manually.

Not all business accounts qualify for CASS — check before you apply. Digital-first banks like Starling and Monzo are CASS-registered for business accounts. Tide is not, meaning you’d need to manually update payment details.

If CASS doesn’t cover your new account, create a list of every party that pays you or that you pay by direct debit. Update them one by one over 4–6 weeks while running both accounts in parallel. It’s a bit of admin, but it’s a one-time task that you only do when you move to a genuinely better account.

FAQ: People Also Ask

Do I need a business bank account as a sole trader in the UK?

You’re not legally required to have one as a sole trader, but it’s strongly recommended. Keeping business transactions separate from personal ones makes your tax return accurate and far less stressful. It also looks more professional to clients who pay by bank transfer.

Can I use my personal bank account for business?

Technically yes, if you’re a sole trader. Most personal account terms and conditions, however, prohibit using personal accounts for business purposes. Your bank can close your account if they discover this. Limited company directors cannot legally use personal accounts for company funds.

Which is better for business: Starling or Monzo?

For most small businesses in the UK, Starling edges ahead on the free tier. It offers more integrations, free UK transfers with no per-transaction fees, and a slightly more robust feature set at no cost. Monzo’s free plan is more limited but works well for very simple sole trader use.

What is the best free business bank account in the UK?

Starling Bank Business Account is widely considered the best free business bank account in the UK in 2026. It charges no monthly fee, no UK transfer fees, and includes accounting software integrations — all at no cost.

Is Tide a good business bank account?

Tide is excellent for fast setup and has a strong invoicing and expense management ecosystem. The free plan’s 20p-per-transfer fee is a meaningful drawback for high-volume businesses. The paid plans offer better value if you transact frequently.

How long does it take to open a business bank account in the UK?

Digital banks like Starling, Monzo, and Tide can approve and open accounts within 24–48 hours in most cases. Traditional high-street banks typically take 1–3 weeks and require more documentation. You’ll usually need proof of ID, proof of address, and your Companies House registration number if you’re a limited company.

The Bottom Line

You don’t need to spend a penny on business banking in 2026. The free options available to UK businesses — particularly Starling, Monzo, and Revolut — are genuinely excellent products that hold their own against paid alternatives.

Start with Starling if you’re unsure. It’s free, full-featured, FSCS-protected, and works for both sole traders and limited companies. If your needs change — more international payments, more cash handling, more credit access — you can always switch.

Open your business account this week, not next month. Every day you mix personal and business finances is a day of admin you’ll eventually have to undo. Take the 10 minutes, get it sorted, and give your business the clean financial foundation it deserves.