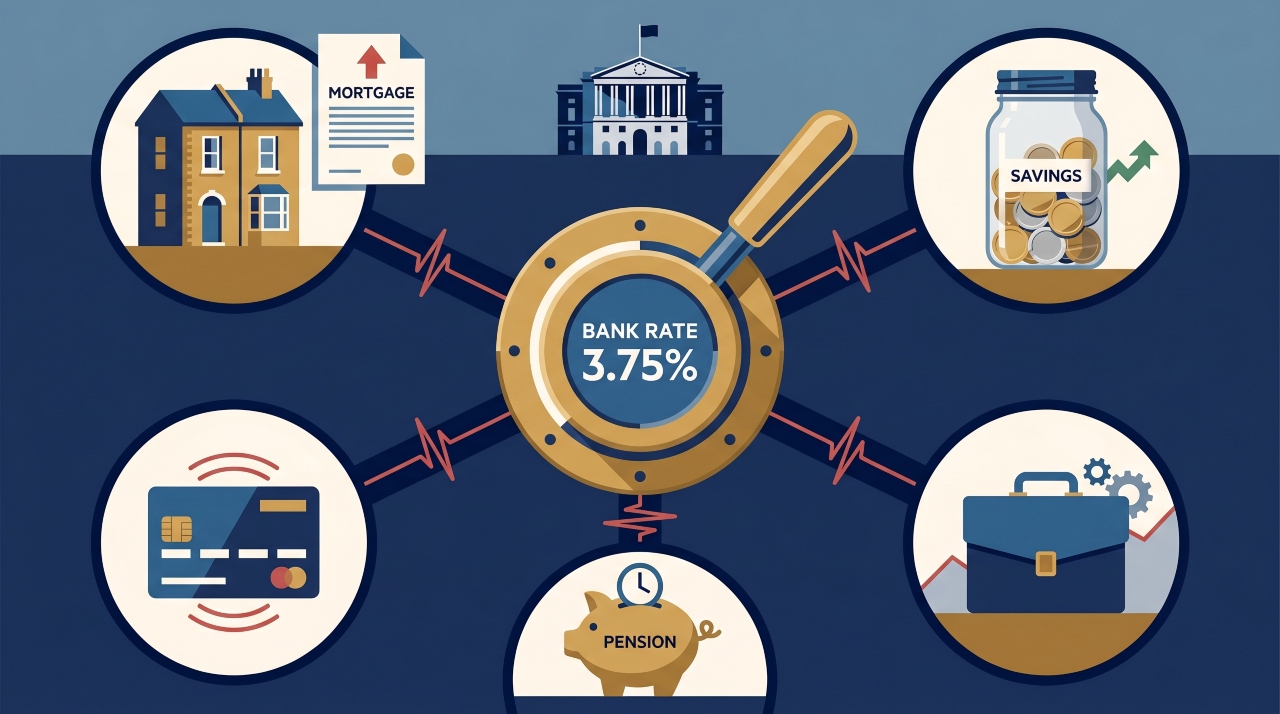

The Bank of England’s base rate sits at 3.75% right now. That single number — set by nine people in a committee room on Threadneedle Street — quietly reaches into your mortgage, your savings account, your credit card bill, your pension, and even the price of your weekly shop.

Most people know rates matter. What most don’t know is exactly how much they matter to their own finances, and what they can actually do about it.

This article breaks down every area of your personal and business finances that UK interest rate changes affect — with real numbers, the current 2026 outlook, and specific actions you can take this month to protect yourself.

What the Base Rate Actually Is (and Why It Moves)

The Bank of England base rate is the interest rate the Bank charges other banks for overnight lending. When that rate moves, the cost of money changes across the entire UK financial system.

The Bank’s Monetary Policy Committee (MPC) meets roughly every six weeks to vote on whether to raise, cut, or hold the rate. Their North Star is a 2% inflation target. Right now, CPI inflation stands at 3.3% — above that target, which is why the MPC voted eight to one at its April 2026 meeting to hold the rate steady rather than cut it.

After peaking at 5.25% in 2023 and 2024, the Bank began cutting rates in August 2024 as inflation pressures eased, reaching the current 3.75% in December 2025. But the expected further cuts in 2026 have been delayed. A new conflict in the Middle East has disrupted energy markets and reversed forecasts, making further cuts increasingly unlikely this year.

The next MPC decision is scheduled for Thursday 18 June 2026.

What this means for you: the environment has shifted from one of falling rates to one of uncertainty. Plans you made assuming steady cuts may need revisiting.

Your Mortgage: The Biggest Hit for Most Households

For most UK households, the mortgage is where rate changes cause the most pain — or relief. But the impact is not the same for everyone, and this is where most generic guides fail you.

Fixed-rate mortgages are the most common deal type. If you’re mid-fix, a rate change does nothing to your monthly payment right now. The hit comes when your deal expires and you remortgage. Around 800,000 fixed-rate mortgages with interest rates of 3% or below are expected to expire every year, on average, until the end of 2027. If yours is among them, the jump in monthly payments will be significant.

Tracker mortgages move directly with the base rate. About 500,000 homeowners have tracker mortgages, and a 0.25 percentage point change typically means around £29 per month on an average outstanding loan balance. That sounds modest, but two or three moves in a year adds up fast.

Standard variable rate (SVR) mortgages are the most expensive place to be. A 0.25 percentage point change for SVR borrowers typically means around £14 per month on the average outstanding loan. The reason the number is lower isn’t because SVR is cheaper — it’s because lenders aren’t required to pass on the full change, and many don’t.

As for current rates: the average five-year fixed mortgage sits at 4.86%, and the average two-year fixed is 4.76%.

What you should do: If your fix ends in the next six months, start shopping now. Most lenders let you lock in a rate three to six months ahead of your deal ending. Given current uncertainty, locking in now rather than gambling on a cut that may not materialise is a reasonable defensive move.

Your Savings: Good News Being Quietly Eroded

Higher rates are good for savers — in theory. In practice, the benefit often arrives slowly and disappears faster than you’d expect.

Easy-access savings rates typically follow the Bank of England base rate, and analysts expect them to trend downwards in 2026 as the base rate remains under pressure. But here’s what the mainstream guides miss: you don’t have to accept whatever your high-street bank offers you.

Smaller banks, building societies, and fintech providers are often quicker than major high-street lenders to offer more competitive rates, and you can still find accounts paying more than 4%. The best easy-access rates and cash ISAs are sitting at institutions most people have never banked with.

A fixed-term savings bond locks in a rate for one or two years. If you believe rates will stay flat or fall, locking in now protects you from that erosion. If rates rise instead, you forgo the upside — but you’ve guaranteed a known return.

The honest trade-off: flexibility versus certainty. A rate at the base rate level may look attractive today, but the real value question is whether inflation — currently 3.3% — is outpacing whatever your savings are earning. Right now, for many easy-access accounts, it still is.

What you should do: Check your savings rate today. If it’s below 4%, search the current best-buy tables and consider moving at least part of your savings to a cash ISA or a competitive easy-access account. A one-hour exercise can add hundreds of pounds per year.

Credit Cards and Personal Loans: The Slow-Moving Pain

Credit card rates in the UK are stubbornly high, and the base rate is only part of the story. Most standard credit cards charge between 20% and 30% APR regardless of what the Bank of England does. The base rate affects the rate at the margin, not the headline number.

Changes to base rate tend to affect new loan rates very gradually, and existing loans on fixed rates are unaffected entirely. The real opportunity here isn’t waiting for the Bank to cut — it’s shifting expensive debt to a 0% balance transfer card while those deals remain available.

Balance transfer deals of up to 35 months at 0% are currently available. If you’re carrying credit card debt at 20%+ and paying it down slowly, moving it to a 0% card for 35 months is the equivalent of getting a massive personal rate cut that no MPC vote will ever give you.

Car finance is a separate category worth watching. Car finance rates can be directly affected by changes to the base rate, but the effect is again gradual. If you’re approaching the end of a PCP deal, the rate on your next agreement may be slightly different from what you’d have found six months ago.

What you should do: If you’re carrying credit card debt, check 0% balance transfer options now. Don’t wait for a base rate cut to reduce your interest burden — the tools to do it yourself already exist.

Your Pension: The Connection Most People Don’t Make

Pensions and interest rates have a relationship that most coverage ignores almost entirely. It matters whether you’re building a pension pot or drawing from one.

If you’re in a defined contribution pension (like a workplace pension), your pot is invested in markets. Lower interest rates can support investment markets, potentially benefiting pension pots invested in shares and bonds — but they can also reduce the income available from lower-risk assets like cash and gilts held within the fund.

If you’re approaching retirement and considering an annuity, the timing of rates matters enormously. Higher interest rates have improved annuity incomes over the past couple of years, allowing those converting pension pots into guaranteed income to secure better deals than in the recent past. If rates fall in 2026, annuity rates may soften — though they’re unlikely to return to the very low levels of a few years ago.

The window to lock in a better annuity rate may narrow if the Bank eventually does cut. If you’re within two years of retirement and considering an annuity, this is worth a specific conversation with a financial adviser.

What you should do: If you’re more than five years from retirement, don’t panic about rate movements — keep contributing and stay invested. If you’re close to converting a pot into income, get a comparison of current annuity rates soon.

Small Business Finances: The Hidden Pressure Point

Most interest rate content focuses entirely on personal finance. If you run a business — even a small one — the impact is different and often more acute.

For businesses, interest rates directly affect cash flow and investment decisions. High rates can increase fixed costs while reducing consumer demand, making it harder to remain competitive.

With the base rate held at 3.75%, businesses can expect borrowing costs to remain fairly steady. But navigating this environment requires careful financial planning, balancing potential cost savings from lower rates with increased operational costs.

The consumer spending effect matters too. Lower interest rates typically lead to increased consumer spending as individuals find it more affordable to borrow and have more disposable income. With rates on hold rather than falling, the consumer spending boost many businesses were expecting hasn’t arrived at the scale predicted at the start of the year.

If your business has a variable-rate overdraft or commercial loan, the rate you’re paying is directly tied to the base rate. Fixed-rate business loans are unaffected until renewal.

What you should do: If your business has a variable-rate facility, review the terms now. Some lenders will allow you to convert to a fixed rate. If you’re planning a significant capital investment that requires borrowing, locking in a rate in the current environment avoids the risk of a future rise.

What Could Change the Picture: Scenarios for the Rest of 2026

The outlook right now is genuinely uncertain, and anyone claiming precise rate predictions for late 2026 is guessing. Here’s what you actually need to watch.

Scenario 1 — Rates held at 3.75% through year-end. This is the current base case. Markets now largely expect the Bank to hold the rate at 3.75% for the rest of the year as they monitor the Middle East conflict and its impact on energy prices. For borrowers on fixed deals, nothing changes. Savers see slow erosion of competitive rates.

Scenario 2 — Rates rise to 4% or higher. Some economists, including Pantheon Macroeconomics, forecast that the MPC could hike rates twice in 2026 if inflation breaches 5%. In a worst case, inflation could hit 6.2% in early 2027, potentially requiring rates as high as 5.25% to combat it. Tracker and SVR mortgage holders would feel this immediately.

Scenario 3 — Cuts resume in late 2026. If the Middle East situation stabilises and energy prices fall, the Bank has indicated there could be scope for rate cuts later in 2026 if inflation falls. Fixed savings rates and fixed mortgages would be unaffected, but variable products would see relief.

The practical takeaway isn’t to predict which scenario plays out. It’s to structure your finances so that you’re not catastrophically exposed to any single outcome.

A Plain-English Action Checklist

Here’s a single reference point covering everything in this article. Run through it once:

| Financial Area | If Rates Rise | If Rates Fall | Do Now |

|---|---|---|---|

| Fixed mortgage | No change until deal ends | No change until deal ends | Check when your fix expires |

| Tracker mortgage | Payments rise | Payments fall | Budget for upside risk |

| SVR mortgage | Payments rise | Payments likely fall | Consider remortgaging off SVR |

| Easy-access savings | Rates should rise | Rates will likely fall | Compare best-buy tables |

| Fixed savings bond | Locked rate | Locked rate | Consider locking in now |

| Credit card debt | Cost of debt unchanged | Cost of debt unchanged | Move to 0% balance transfer |

| Annuity (retirement) | Better rates available | Rates may soften | Shop now if close to retirement |

| Business variable loan | Costs rise | Costs fall | Review terms, consider fixing |

The One Thing Most People Miss

Every article you’ll read about UK interest rates focuses on what the Bank might do next. That’s the wrong question for most people.

The right question is: what would happen to your finances if rates rose 0.5% from here? And are you comfortable with that answer?

If you’re on a tracker and the answer is “I’d struggle,” that’s a signal to remortgage. If your savings are sitting in a high-street account earning 2% while inflation runs at 3.3%, the base rate isn’t your problem — inertia is.

The next base rate decision is scheduled for 18 June 2026. Between now and then, the single best financial move most UK households can make isn’t waiting for that announcement — it’s checking their mortgage deal, their savings rate, and their debt position, and acting on whichever one is leaking money.

That takes an afternoon. The Bank of England has your attention right now. Use it.

This article is for informational purposes only and does not constitute financial advice. Always consider speaking with an independent financial adviser before making significant financial decisions.