Nearly 40% of small businesses will file an insurance claim within the next 10 years, yet most new business owners have no idea which policies the law actually requires them to carry. The difference between required and recommended coverage can mean thousands of dollars in premiums and the difference between legal compliance and serious penalties.

This guide breaks down exactly which insurance policies your business must have based on your state, industry, and number of employees. You’ll also learn which optional coverages protect you from the most common business risks so you can make smart choices without overpaying.

Who Needs This Information Most

If you recently formed an LLC, incorporated a business, or hired your first employee, this article is for you. Maybe you’re comparing insurance quotes and wondering why some agents push certain policies while others say they’re optional. Or perhaps you received a letter from your state requiring proof of coverage and you’re not sure what that means.

New business owners face the biggest confusion around insurance requirements because the rules change based on your location, industry, and business structure. Getting clarity now prevents expensive mistakes later.

What Makes Business Insurance Legally Required

Insurance becomes mandatory through three main channels: state laws, federal regulations, and contractual obligations. Understanding which category applies to your business helps you separate true legal requirements from smart recommendations.

State laws create most mandatory insurance requirements. Every state except Texas requires businesses with employees to carry workers compensation insurance. The threshold varies, with some states requiring coverage the moment you hire your first employee, while others set minimums at three or five employees. California, for example, mandates workers comp even if you have just one part time worker.

Federal law adds requirements for specific situations. Businesses with 50 or more full time employees must offer health insurance under the Affordable Care Act. Companies that operate vehicles for business purposes may need commercial auto insurance to comply with federal transportation regulations. Federal contractors often face additional insurance mandates written into their contracts.

Contractual requirements come from business relationships rather than government agencies. Your commercial lease probably requires general liability insurance naming your landlord as an additional insured. Clients who hire you for projects often demand proof of professional liability coverage before signing contracts. Lenders typically require commercial property insurance before approving business loans.

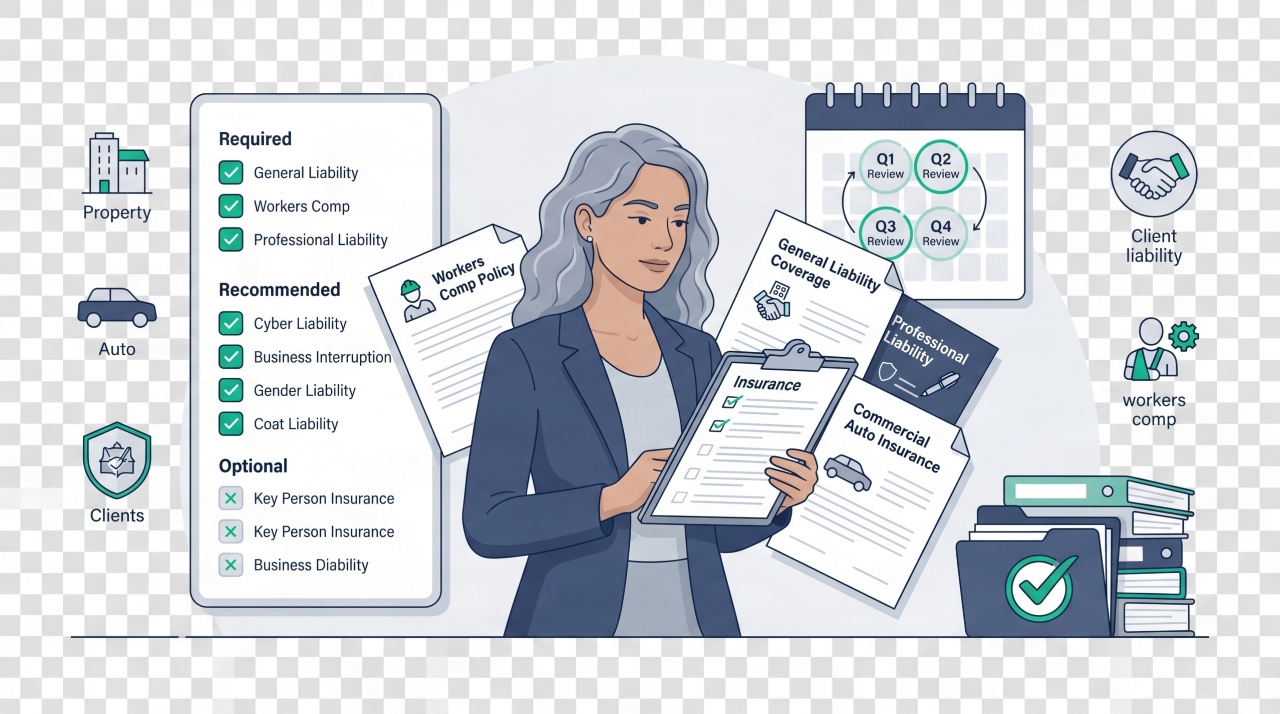

The Seven Types of Business Insurance You’ll Encounter

Workers Compensation Insurance

This policy covers medical expenses and lost wages when employees get injured or sick because of their job. Almost every state requires it once you hire employees, and the penalties for skipping it include fines up to $100,000 plus potential criminal charges in some states. Check your state specific workers compensation requirements through the Department of Labor to confirm your threshold.

Workers comp requirements kick in at different employee counts depending on where you operate. Georgia requires it when you have three or more employees. New York and California require it starting with your first hire. Sole proprietors and partners can usually exclude themselves from coverage, but employees must be covered.

The cost runs between $0.75 and $2.75 per $100 of payroll on average, though high risk industries like construction pay significantly more. Most states let you buy coverage through private insurers or state operated funds. A few states like North Dakota and Washington operate monopolistic systems where you must buy from the state fund.

General Liability Insurance

General liability covers property damage and bodily injury claims from third parties. While rarely required by law, most commercial leases and client contracts make it mandatory for practical purposes. This policy pays when a customer slips in your store, when your work damages client property, or when your advertising injures someone’s reputation.

Coverage typically starts at $1 million per occurrence with $2 million aggregate limits. Premium costs range from $400 to $1,500 annually for low risk businesses like consultants or retailers. Service businesses that work on client sites often pay more because of higher exposure to property damage claims.

You can often skip this coverage if you work from home with no client visits and provide only digital services. The moment you meet clients in person, rent commercial space, or perform physical work, general liability becomes essential even if not legally mandated.

Professional Liability Insurance (Errors and Omissions)

Professional liability protects against claims that your advice, services, or professional work caused financial harm to a client. Lawyers, accountants, architects, consultants, and healthcare providers face the highest demand for this coverage. Many state licensing boards require it for certain professions, and most sophisticated clients won’t sign contracts without proof of coverage.

This policy covers legal defense costs and settlements when clients sue over mistakes, missed deadlines, or professional negligence. A single lawsuit defense can cost $50,000 even if you win, making this coverage valuable beyond any legal requirement.

Annual premiums vary widely based on your profession and revenue. Consultants might pay $500 to $1,500 per year for $1 million in coverage. Medical professionals and lawyers often pay $5,000 to $15,000 or more due to higher claim frequency and severity.

Commercial Auto Insurance

Any vehicle titled to your business or used regularly for business purposes needs commercial auto coverage. Personal auto policies specifically exclude business use, meaning your personal insurance won’t pay if you crash while making deliveries or visiting client sites.

State laws require minimum liability coverage amounts, typically ranging from $25,000 to $50,000 per person for injuries. Smart business owners carry much higher limits since serious accidents easily exceed state minimums. If employees drive their own cars for business errands, you need non owned auto coverage to protect against claims that exceed their personal policies.

The legal requirement applies the moment you use a vehicle for business purposes. Occasional business use of your personal car sits in a gray area, but regular use or vehicle ownership under your business name creates a clear mandate.

Unemployment Insurance

Businesses with employees must pay unemployment insurance taxes in all 50 states. This isn’t traditional insurance you buy from a carrier. Instead, you pay taxes to your state unemployment fund based on your payroll and claims history.

Requirements typically kick in once you pay $1,500 or more in wages during a calendar quarter or when you have at least one employee for 20 different weeks in a year. Each state sets its own wage base and tax rates. New employers usually pay a standard rate until they build a claims history.

Failing to register and pay unemployment taxes results in penalties, back taxes, and interest charges. States aggressively pursue unpaid unemployment taxes because these funds pay benefits to laid off workers. You register through your state’s employment or revenue department, usually during your initial business registration process. The SBA breaks down unemployment insurance tax obligations and registration steps by state.

Disability Insurance

A handful of states require businesses to provide short term disability coverage for employees. California, Hawaii, New Jersey, New York, and Rhode Island operate mandatory disability insurance programs. Puerto Rico also requires it.

These programs replace a portion of wages when employees can’t work due to non work related illness or injury. Employers either pay into a state fund or purchase private coverage that meets state requirements. Coverage usually replaces 50% to 70% of wages up to a weekly maximum.

If you operate outside these five states, disability insurance remains optional. Many businesses offer it as a voluntary benefit to attract quality employees, but no legal mandate exists in most locations.

Commercial Property Insurance

No law requires commercial property insurance, but practical necessity makes it mandatory for most businesses. Mortgage lenders require it on owned buildings. Landlords require tenant’s property coverage in lease agreements. The risk of losing your equipment, inventory, and furnishings to fire, theft, or storms makes this coverage essential even without legal mandates.

Commercial property policies cover your building (if you own it), equipment, inventory, furniture, and fixtures. Most policies also include business interruption coverage that replaces lost income when property damage forces you to close temporarily.

Costs depend heavily on your location, building age, construction type, and coverage limits. A small office might pay $500 to $1,000 annually. Retail stores with significant inventory often pay $1,500 to $3,000 or more.

What Most Articles Get Wrong About Business Insurance Requirements

Most guides treat insurance requirements as if they’re the same for all businesses, but your specific situation creates unique mandates. A tech consultant working from home faces completely different requirements than a restaurant owner or construction company.

The biggest mistake new business owners make is asking “what insurance do I need” without specifying their state, industry, and business structure. A graphic designer operating as a sole proprietor in Texas has zero legally required insurance. That same designer incorporated in California with two employees suddenly faces workers comp mandates, unemployment insurance requirements, and likely contractual demands for general and professional liability.

Start by identifying your specific situation: your state of operation, your legal structure (sole proprietor, LLC, corporation), your number of employees, your industry, and whether you operate vehicles or own commercial property. Then research requirements that match those specific factors. Generic advice wastes your time and often misses critical requirements or pushes unnecessary coverage.

How to Identify Your Actual Requirements

Start with your state’s department of labor or insurance website. Search for “business insurance requirements” plus your state name. Look specifically for workers compensation rules, unemployment insurance registration, and any industry specific mandates. Most states publish clear guides for new employers.

Next, review any commercial leases, client contracts, or loan agreements you’ve signed. These documents spell out contractual insurance requirements. Look for sections titled “insurance” or “indemnification.” Note the required coverage types and minimum limits.

Contact your professional licensing board if your work requires a state license. Accountants, contractors, healthcare providers, real estate agents, and many other licensed professionals face profession specific insurance mandates. Your licensing board can tell you exactly what you need.

Get quotes from three insurance agents and ask each one to identify mandatory versus recommended coverage for your specific business. Compare their answers. If all three mention the same requirements, you’ve found your legal mandates. Coverages where recommendations differ are usually optional, and you can decide based on your risk tolerance and budget.

Take These Steps This Week

Call your state’s labor department and ask about employer insurance requirements—you can find your state agency contact information through professional licensing requirements and business registration resources on USA.gov. You can usually find the number on your state government website. You can usually find the number on your state government website. Ask specifically about workers compensation thresholds, unemployment insurance registration, and disability insurance if applicable. This single call clarifies most legal requirements.

Pull out your lease agreement and any client contracts you’ve signed. Highlight every insurance requirement you find. Make a list with coverage types and required limits. If something seems unclear, email your landlord or client for clarification.

Get quotes from at least two insurance agents or brokers. Tell them your state, industry, business structure, employee count, and revenue. Ask them to separate legally required coverage from optional policies. Request quotes for just the required coverage, then ask what adding recommended policies would cost.

Set calendar reminders to review your insurance annually. Requirements change when you hire employees, move to a new state, sign big client contracts, or grow revenue significantly. What you need today might not match what you need in 12 months.

Making Smart Coverage Decisions Without Overpaying

Business insurance requirements create your baseline coverage, but smart protection usually means adding one or two optional policies that match your biggest risks. The goal is protecting your business and complying with the law without paying for redundant coverage or policies that don’t match your actual exposure.

Focus first on meeting all legal and contractual requirements. Then evaluate optional coverage based on your specific risks. Service businesses benefit most from professional liability. Product sellers need product liability coverage. Businesses with significant equipment or inventory should prioritize property insurance.

Get the mandatory coverage in place immediately, compare quotes to ensure competitive pricing, and review your needs every year as your business grows and changes. Insurance requirements evolve with your business, so treating this as a one time decision leaves dangerous gaps or wastes money on coverage you’ve outgrown.