Over 800,000 new businesses registered in the UK in 2023 alone — that’s roughly one new business every 39 seconds. Yet nearly half of all new UK businesses don’t survive past their fifth year. The difference between those that thrive and those that don’t usually comes down to one thing: preparation.

If you’re thinking about how to start a business in the UK, you’ve already taken the most important step — you’re asking the right questions. This guide walks you through every stage, from choosing your idea to your first 30 days of trading. You’ll also get an honest look at the costs, the common mistakes, and what most other guides forget to mention.

Is Starting a Business in the UK a Good Idea Right Now?

The short answer is yes — and the data backs it up. The UK has one of the most accessible business registration systems in the world. You can legally register a company online in as little as 24 hours, and the process costs as little as £12 through Companies House online registration.

The UK also ranks highly in global indexes for ease of doing business, strong legal protections, and access to skilled talent. For anyone outside the UK considering launching there, you don’t need to be a British citizen. Non-UK residents can register and run a UK limited company, which makes it an attractive option for international entrepreneurs.

That said, starting a business isn’t effortless. You’ll face competition, early cash flow pressure, and the mental weight of making decisions alone. This guide won’t sugarcoat any of that.

1: Validate Your Business Idea First

Before you register anything, spend time validating your idea. This is the step most people skip — and it’s the one that saves you the most money.

Validation means checking whether real people will actually pay for what you’re offering. You don’t need a fancy survey tool. Talk to 10–20 potential customers, ask them what they struggle with, and see if your idea solves that problem.

A simple way to test demand is to create a basic landing page describing your product or service, then run a small paid ad (even £50 worth) to see if people click and sign up. If nobody’s interested at that stage, that’s valuable information — and it costs you far less than a full launch.

2: Write a Simple Business Plan

You don’t need a 40-page document. A business plan is really just your thinking made visible on paper. It helps you spot problems before they cost you money.

Your plan should cover: what you’re selling, who your customers are, how you’ll reach them, what your startup costs are, and how you’ll make money. The GOV.UK business plan guidance offers free templates that are genuinely useful for first-time founders.

Keep it short — even two pages works for most small businesses. You can always expand it later when you apply for funding or investment.

3: Choose the Right Business Structure

This is one of the biggest decisions you’ll make, and it affects your taxes, your liability, and how you’re seen by customers and investors.

Here are your main options in the UK:

| Structure | Best For | Tax Setup | Personal Liability |

|---|---|---|---|

| Sole Trader | Freelancers, low-risk | Income Tax + NI | Unlimited |

| Limited Company | Growth-focused, investors | Corporation Tax | Limited |

| Partnership | Two or more founders | Income Tax + NI | Shared/Unlimited |

| LLP | Professional services | Income Tax + NI | Limited |

Sole trader is the simplest structure. You register with HMRC, keep all profits after tax, and there’s almost no paperwork to set up. The downside is that you’re personally liable for any debts the business takes on.

Limited company is the most popular choice for anyone who plans to grow, hire staff, or attract investment. Your personal assets are protected from business debts, and you’ll often pay less tax overall once you’re earning above around £30,000 per year. You register with Companies House, file annual accounts, and pay corporation tax (currently 19–25% depending on profits as of 2024).

Most people starting out go sole trader first, then switch to limited company once they’re making consistent income. That’s a perfectly valid route.

4: Register Your Business

Once you’ve chosen your structure, registration is straightforward.

Sole trader: Register for Self Assessment on HMRC Self Assessment registration. You must do this by 5 October in your business’s second tax year.

Limited company: Register through Companies House. You’ll need a company name (it must be unique), a registered UK address, at least one director, and details of shareholders. The online process takes about 15–30 minutes and costs £12. You’ll get a certificate of incorporation usually within 24 hours.

What about VAT? You must register for VAT once your taxable turnover hits £90,000 in a 12-month period (the threshold as of 2024). You can also register voluntarily before that, which can make your business look more established and lets you reclaim VAT on business purchases.

5: Sort Your Finances From Day One

Getting your money sorted early saves you enormous stress later. Open a dedicated business bank account as soon as your business is registered. Mixing personal and business finances is one of the most common mistakes new business owners make — and it creates a nightmare at tax time.

Most UK high-street banks offer business accounts, but challenger banks like Starling, Tide, and Monzo Business offer faster setup, lower fees, and strong app-based accounting features. Many have free plans for small businesses.

You’ll also want basic bookkeeping software. Tools like Xero, QuickBooks, or FreeAgent (free with some NatWest and RBS accounts) connect to your bank and make invoicing and tax reporting much easier.

Set aside 20–25% of every payment you receive into a separate savings account for tax. It sounds simple, but it’s one of the habits that separates stressed business owners from calm ones.

6: Understand Your Tax Responsibilities

Tax doesn’t need to be scary, but you do need to know what’s coming. Here’s what most UK business owners deal with:

- Self Assessment / Corporation Tax: Sole traders file a Self Assessment tax return each year. Limited companies file a Corporation Tax return with HMRC.

- National Insurance: Sole traders pay Class 2 and Class 4 NI contributions. Directors of limited companies typically take a mix of salary and dividends to reduce NI liability.

- PAYE: If you hire employees, you’ll need to register as an employer and run payroll through HMRC’s PAYE system.

- VAT: If you’re VAT-registered, you’ll file quarterly VAT returns.

If tax feels overwhelming, hiring a UK-based accountant for even a few hours a year is money well spent. The average UK small business accountant charges between £500–£1,500 per year for basic services.

7: Protect Your Business Legally

Many new business owners skip legal protection until something goes wrong. Don’t be that person.

At minimum, you should look at:

- Business insurance: Public liability insurance is essential if you deal with customers in person. Professional indemnity insurance protects you if a client claims your advice or service caused them a loss.

- Contracts: Always use a written contract with clients and suppliers. You can find affordable legal templates through services like Rocket Lawyer or LawDepot.

- Intellectual property: If you’ve created a brand, logo, or product, consider registering a trademark with the UK Intellectual Property Office. It costs from £170 and protects your brand legally.

These aren’t just formalities — they protect everything you’re building.

8: Find Funding If You Need It

Not every business needs external funding, but if yours does, the UK has solid options.

Bootstrapping (using your own savings) is the most common starting point. It keeps you in control and forces you to be lean.

Start Up Loans is a UK government-backed scheme offering loans of £500–£25,000 at a fixed 6% interest rate, plus free mentoring. You can apply through the British Business Bank’s Start Up Loans scheme regardless of your background or credit history.

Grants are available through local councils, Innovate UK, and sector-specific bodies. They don’t need to be repaid, but they’re competitive and often slow to access.

Angel investors and venture capital are typically more relevant once you have proven revenue and a scalable model.

9: Build Your Online Presence

You don’t need a perfect website on day one, but you do need a credible digital footprint. Most customers will search for you online before they contact you.

At a minimum, set up:

- A simple website (Squarespace, Wix, or WordPress work well for beginners)

- A Google Business Profile (free, and essential for local visibility)

- At least one active social media profile relevant to your audience

Your website doesn’t need to be complex. A clear homepage explaining what you do, a way to contact you, and a few lines about your background is enough to start. You can expand as you grow.

Want help thinking through how to get found online? Our guide on SEO basics for small business owners walks you through the essentials without the technical jargon.

10: Plan Your First 30 Days

Most business guides stop at registration. This is where things get real.

Your first 30 days should focus on three things only: getting your first customer, telling everyone you know what you now do, and setting up simple systems so you can repeat the work.

Tell your network on day one. Post on LinkedIn, email your contacts, and tell people in person. Word of mouth is still the fastest and cheapest way to get your first clients, especially in service-based businesses.

Aim for your first paying customer within 30 days. Even one small job proves demand, gives you confidence, and generates a testimonial. Don’t wait until everything feels ready — it never will.

For a deeper look at which type of business might suit you best, check out our guide on best business ideas to start in the UK.

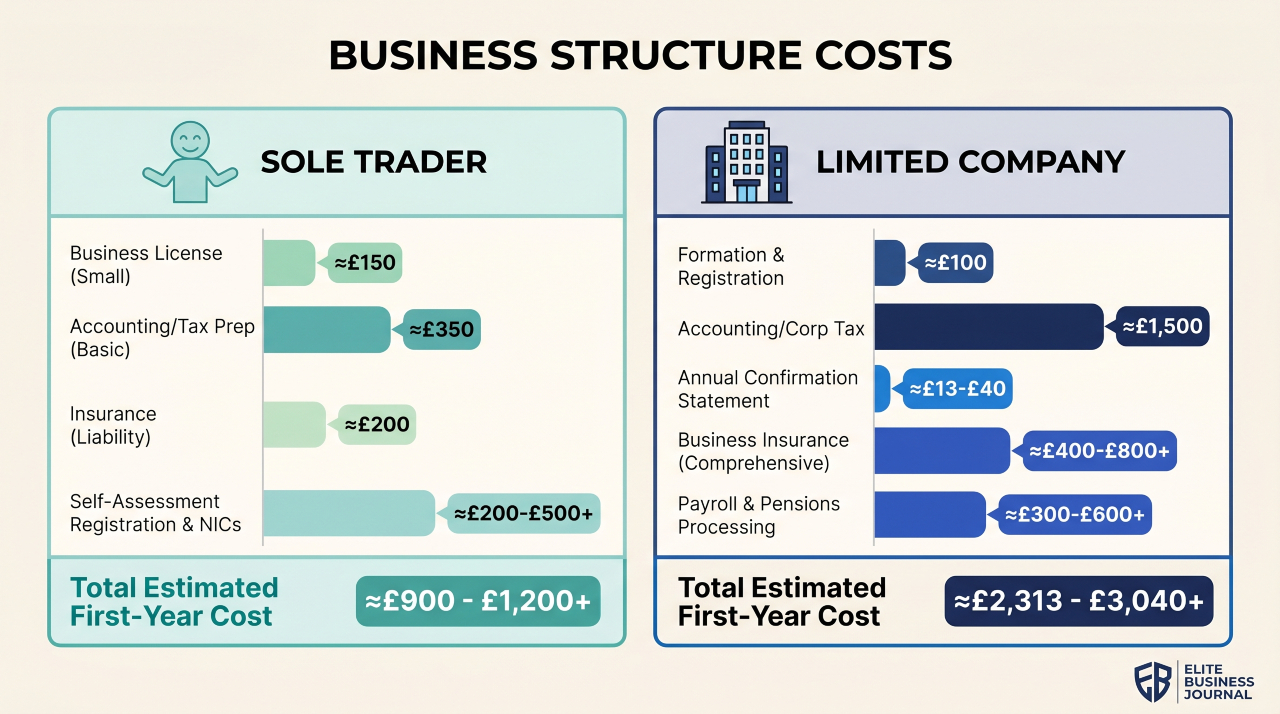

What Does It Actually Cost to Start a UK Business?

Let’s be honest about money. The cost of starting depends hugely on your business type, but here’s a realistic breakdown for the two most common routes:

Sole trader (service-based, e.g. freelance designer or consultant):

- HMRC registration: Free

- Website: £100–£300/year

- Business bank account: £0–£10/month

- Accounting software: £0–£30/month

- Insurance: £100–£300/year

- Total first-year cost: £200–£700

Limited company (product or tech-based):

- Companies House registration: £12

- Accountant: £500–£1,500/year

- Website and branding: £500–£2,000

- Business insurance: £200–£600/year

- Product development or inventory: Varies widely

- Total first-year cost: £1,500–£5,000+

These numbers assume you’re keeping costs lean. You can spend much more — but you don’t have to.

Can a Non-UK Resident Start a Business in the UK?

Yes — and this surprises many people. You don’t need to be a UK citizen or resident to register a UK limited company. You’ll need a registered UK address (a virtual office service can provide this), and you must comply with UK tax law.

Many international entrepreneurs use UK company registration to access UK and European markets, build credibility, and open a GBP bank account. It’s a legitimate and popular strategy for global founders.

You will likely need an accountant familiar with cross-border tax issues, particularly if you’re not a UK tax resident. This is one area where professional advice is genuinely worth the cost.

FAQ: Common Questions About Starting a Business in the UK

What is the first step to starting a business in the UK?

The first real step is validating your idea — making sure real people want what you’re planning to sell. After that, you choose your business structure, then register with either HMRC (sole trader) or Companies House (limited company). Jumping straight to registration without validation is one of the most common early mistakes.

How much does it cost to start a business in the UK?

It depends on your business type. A solo freelancer can start for as little as £200–£700 in their first year. A product-based or limited company might spend £1,500–£5,000 or more. The registration fee itself is as low as £12 for a limited company, or free for sole traders.

Do I need to register my business in the UK?

Yes, in most cases. If you earn money from self-employment, HMRC requires you to register for Self Assessment. If you set up a limited company, you must register with Companies House. Operating without registering can result in fines and backdated tax bills.

Can a foreigner start a business in the UK?

Absolutely. Non-UK residents can register and run a UK limited company. You’ll need a UK registered address and must comply with UK corporate tax rules. Many international founders use a virtual office address for this purpose.

What business structure should I choose in the UK?

For most beginners, sole trader is the simplest starting point. If you plan to scale, take on investors, or want personal liability protection, a limited company is the better choice. Most business owners switch from sole trader to limited company once their income consistently exceeds around £30,000 per year.

How long does it take to register a business in the UK?

Registering a limited company online through Companies House typically takes 24–48 hours. Sole trader HMRC registration is processed in a few days, though you can start trading immediately. VAT registration can take 30–40 working days if done by post, but online registration is much faster.

The One Thing Nobody Tells You About Starting a Business

Here’s something most guides won’t say: the hardest part of starting a business isn’t the paperwork. It’s the uncertainty. You won’t know if it’ll work. You’ll second-guess yourself constantly. You’ll wonder if you’re making the right moves.

That’s completely normal, and it doesn’t go away — but it does get easier as you build momentum and start seeing results. The founders who succeed aren’t the ones who feel most confident at the start. They’re the ones who take the next step anyway.

You’ve already done that by reading this far. Now pick one action from this guide — just one — and do it today. Whether that’s validating your idea, researching your business structure, or simply writing down what problem you want to solve.

That single step is how every business in the UK started.